Crypto 101 Ep 1: Understanding The Technology That Powers Cryptocurrencies

Posted by Anushiem Chidera on August 15, 2022 in Guide/Series

Crypto 101 Ep 1: Understanding The Technology That Powers Cryptocurrencies

As Nigerians, we have seen cryptocurrencies as a topic, rise from relative obscurity to mainstream popularity. For different reasons, Nigerians have fallen in love with the idea of a decentralized digital currency. But do you know what technology makes cryptocurrency even exist? After reading this article, you’ll learn all the intricacies of blockchain technology.

A Brief History of Blockchain Technology

The traditional economy as we know it has several issues such as zero transparency, high card transaction fees, and the high population of 1.7 billion unbanked adults (almost one in three adults are unbanked in Nigeria).

To solve these problems, Satoshi Nakamoto developed the first blockchain database and developed bitcoin, the first ever cryptocurrency. Interestingly, Satoshi’s identity has never been uncovered— no one can say with certainty if he was an individual or a group of people.

A back story: Before Satoshi, in 1991, Scott and Stuart created a solution using cryptography for time-stamping digital documents to keep them secure from backdating or data tampering. Future computer scientists like Satoshi took inspiration from their work, leading to the creation of blockchain and, by extension, cryptocurrencies.

With this technology, more people had easy access to send and receive payments seamlessly and securely. Here is everything you need to know about revolutionary Blockchain technology.

Ready to learn?

Let’s get into it!

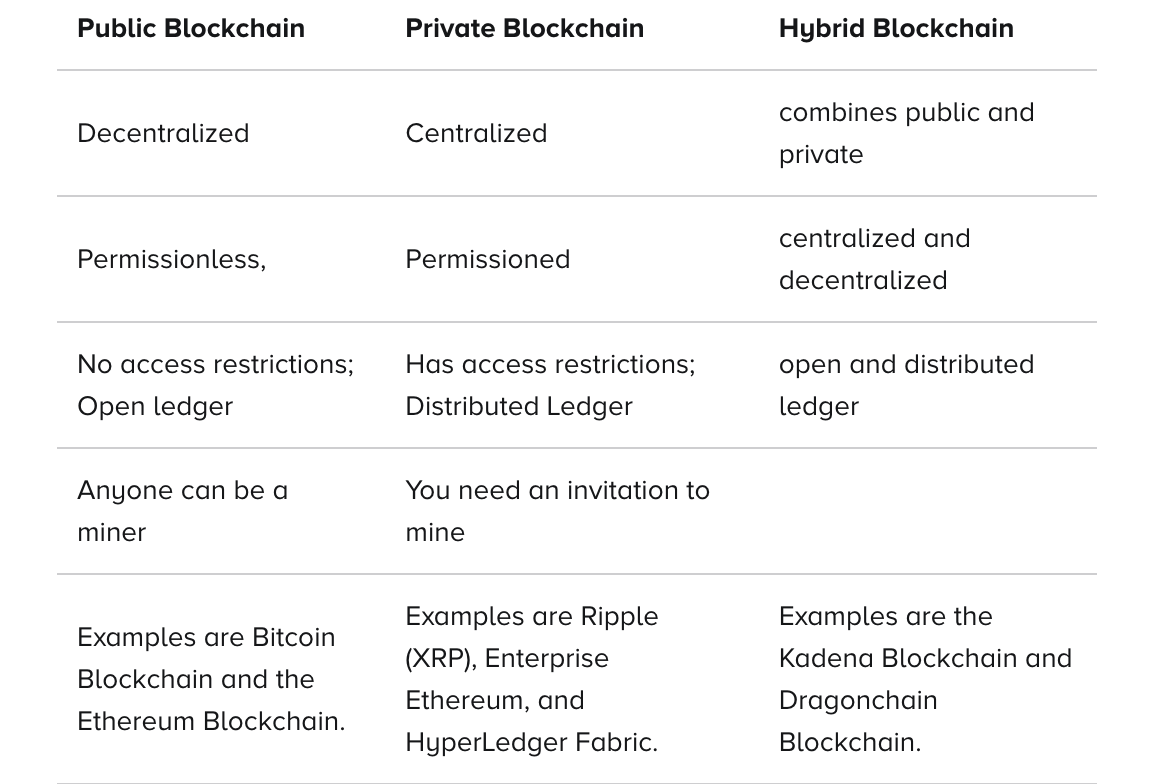

Types of Blockchain

Although every blockchain is similar in that they are a group of nodes working on a peer-to-peer network system, certain distinguishable factors make it necessary to group them. The image below is an apt classification of blockchains:

How Does Blockchain Work

To explain this, let’s do an illustration with some random people we will call Danladi, Ajadi, and Amadi. Assuming Danladi and Ajadi are to send 25 USDT each to Amadi, Amadi already has 250 USDT in his crypto wallet. As a result, Danladi has 50 USDT in his wallet reserve, while Ajadi has 100 USDT in his wallet. When Danladi sends 25 USDT to Amadi, a record is created in the form of a block, and the details of the transaction between them are permanently documented in this block. This record also holds the amount of USDT each person owns. So, after Danladi’s transaction, Amadi has 275 USDT while Ajadi has 100 USDT. When they both send their 25 USDT, an alphanumeric record is created in the form of a block for each transaction. These blocks are then linked to each other in a sequence (hence the name ‘block-chain’) as each block takes reference from the previous one for the number of USDT each person owns. This chain of records (or blocks) is called a ledger, and each ledger is shared among all three friends, making it a ‘Public Distributed Ledger.’ This is how a blockchain works and it is the concept that underpins the concept. Now that you understand the concept of blockchain, how exactly can this technology be beneficial?

Uses of the Blockchain

Blockchain technology can be applied to different use cases, including gaming, financial services, supply chains, security, and even domain names. Here are a few examples of these use cases for blockchain across industries.

Seamless Payments and Cryptocurrencies As stated earlier, cryptocurrencies are the most common and most prominent use case of blockchain technology. Crypto payments solve cross-border payments since they are not restricted by geographical locations. With an active internet connection, anyone can transact with crypto anywhere, anytime. Whether their national governments prohibit crypto transactions or not.

Bringing this use case home, Africa has an issue with the interoperability of currencies. On other continents, you can easily send money from country to country without any hitches.

The same can’t be said for Africa. South Africans can’t spend their Rands and Nigerians must buy Shillings if they want to spend in Kenya. With crypto, this problem does not exist. The currency is valid wherever you are.

Many businesses worldwide now accept stablecoins, a non-volatile form of cryptocurrencies as a payment method. African businesses like Basqet, WorldCore, and Nguvu Health now accept crypto payments from all over the globe. If you run a business and want to integrate crypto into your list of payment methods, follow these easy steps:

- Understand cryptocurrency payments

- Set up a wallet on an exchange or purchase a more secure cold wallet (a cold wallet is a hardware device used to store cryptocurrencies). You can set up a wallet on exchanges like Binance, Coinbase, and many others. You can purchase cold wallets on Amazon or Ledger.

- Integrate crypto payments into your online checkout using platforms like Coinbase Commerce and BitPay.

- Offer in-person payments.

Smart Contracts

A smart contract is a piece of code that automatically executes a command if a pre-programmed condition is met. They are distributed, and everyone within the network has access to them, which means there are no discrepancies. They are also used to remove human error and/or manipulation in legalizing contracts and prevent both parties from defaulting.

Smart contracts are coded on the blockchain and cannot be altered forever. This means once the terms and conditions for agreements are set, neither party can go back on their word. One of the amazing use cases for Smart Contracts is it ensures digital art creators get paid for their work.

With smart contracts, digital artists can encode royalties into their work. This ensures that they get paid immediately anytime their work is sold to buyers or consumers.

Advantages of Blockchain

Since Satoshi first published the bitcoin whitepaper in 2008, blockchain adoption has continued to grow. Industries in finance, gaming, health, and artificial intelligence have adopted blockchain technology due to its features that allow it to deliver cost-saving solutions.

Permissionless System

Due to the permissionless structure of blockchain technology, transactions can take place without interference from other parties.

For instance, when you use a standard payment system to make a payment, more parties than just you and your bank are typically required for the transaction to be completed. In this kind of transaction, third parties like a payment processor or credit card firms (Visa, Mastercard) are essential.

As everyone on the Blockchain can see what is happening (distributed ledger), and as long as the miners can approve your transaction, blockchain technology eliminates the need for any third parties to be involved in your transaction.

The Blockchain is considered a "trustless system" because of this.

Proof of work or proof of stake is used to validate new entries on the Blockchain in Ethereum, Bitcoin, stablecoins, and other cryptocurrencies that operate on it.

This eliminates the need to get approval from a single entity because any miner who has proof of work or proof of stake can approve your transaction.

By removing third parties and intermediaries, Blockchain reduces the cost of processing payments and transaction fees.

Security

Blockchain technology can greatly enhance data security while assisting you in preventing employee or business partner fraud. The security of your data is of utmost importance to you as a business owner. End-to-end encryption is used to protect data created on the blockchain, which cannot be changed.

With the use of Blockchain technology, your company may build a smart contract on the Blockchain and transmit it to a business partner. The recipient can only activate the contract when all the conditions are met. These data are safe and secure since they are shielded from your end to theirs and cannot be changed.

Your financial records can be saved on the Blockchain as well. This will stop employees with ulterior motives from covering up questionable transactions or manipulating the company's balance sheet. Hackers cannot alter your data once it is stored on the Blockchain. Since every user has a copy of the ledger, the hacker needs to hack every user to change the data.

The video below is a helpful guide on how blockchain can help secure your business.

https://www.youtube.com/watch?v=3FCizoynRf8

Because data is not concentrated at one location, decentralization of the blockchain significantly lessens the likelihood of a technical malfunction or network collapse. How does this affect businesses, then?

It implies that you are free from having to worry about network availability or security. You do not have to worry if PayPal’s site is down or if VISA cannot process your transaction at that time. There is almost little risk that network unavailability, which sometimes happens with traditional banks, will cause your payment process to be interrupted.

Conclusion

Blockchain technology has valid use cases. Now is the time to leverage blockchain technology and create better economic opportunities and improve your outcomes.